Evolution AB (EVVTY) May Update: Why I can't Stop Buying

60% Of My Portfolio and I'm Still Buying at $66

As of April 2026 I hold a long position in Evolution AB (EVVTY). About 60% of my portfolio. This article is for informational and educational purposes only and is not financial advice. Investing in stocks is risky.

I have received a lot of questions and requests to do an update on Evolution. Here is a link to my article in December. My conviction has only strengthened, and this is now around 60% of my portfolio with a cost basis is $64.52. I will first recreate a similar Investment Thesis and then I will go through updates from since my original post. If you enjoy the article help me out by liking and subscribing. Thank you!

Investment Thesis

Evolution AB is the clear market leader in B2B live dealer gaming with over 60% market share. It operates as the essential infrastructure layer for the fastest growing segment of online gambling. No expensive marketing budget, no billions burned on free bets. A perfect business model with net income margins that sit around 50%.

This has been a phenomenal growth company that’s hit a speed bump recently. Revenue grew from $428M in 2019 to roughly $2.4B in 2025, a six-year CAGR of about 33%. Capital allocation is superb. The company recently cancelled its dividend to spend all available cash on buybacks, a move that is brilliant at these prices. When your stock trades at 11x earnings, every dollar spent on buybacks retires shares at a massive discount to intrinsic value. Rather than mailing cash out the door, management is using all excess income to aggressively shrink the share count. Shares outstanding shrunk about 4% last year and that pace should accelerate with the full earnings stream now directed at repurchases. Every remaining share owns more of the business than it did a year ago.

The Q1 2026 results are much better than the headline 1.5% revenue decline suggests. Because Evolution reports in euros and a significant portion of its revenue comes from dollar denominated markets, the strong euro masked what was really happening underneath. On a constant currency basis, Q1 revenue actually grew 6.8% year over year. This is a company going through a rough patch while still growing at almost 7% while the market prices it at 11 times earnings.

The regional breakdown makes the story even clearer. North America delivered 21% year over year growth in US dollars and hit an all time revenue high. Latin America grew 29% and also hit an all time high. Asia posted its second consecutive quarter of sequential growth, suggesting the piracy cleanup might be beginning to stabilize. The weak spot is Europe, where regulatory volatility and declining channelization rates dragged the region down nearly 6% quarter over quarter. But even with Europe struggling, the company still earned EUR 252M in net income in a single quarter while maintaining a 49% net margin.

Like we said earlier the board cancelled the 2025 dividend entirely, stating that cash dividends are not the best way to create long term shareholder value at this time. With EUR 1.2B in cash on the balance sheet and essentially zero debt, that capital is being redirected toward aggressive share buybacks and global expansion into the US and Latin America. For a stock trading at 11 times earnings, I would rather see every available dollar go into buybacks anyway. This makes me like the stock more.

Even with Europe maturing and currently contracting and Asia still stabilizing, the overall growth picture for Evolution remains very attractive. The online gambling market is projected to grow at 10% or more annually through 2030. North America has iGaming legal in only about 7 states with giants like New York and California still on the sideline. Latin America is just getting started with Brazil’s regulated market barely a year old and Colombia and Argentina expanding. Asia is showing early signs of recovery after more than a year of piracy driven disruption. And management continues to invest aggressively, with 110 new game releases planned for 2026 including a global exclusive partnership with Hasbro to build MONOPOLY branded live casino and slot games. Even if Europe stays flat for years, the combined growth from these other regions gives Evolution a clear path to double digit revenue growth, and management’s long-term ambition remains to grow at least in line with the overall market in every region they operate in.

Summary:

• Clear market leader with 60% market share

• 6-year revenue CAGR of roughly 33% (2019 to 2025)

• Operating margins near 58%, net income margins above 50%

• Aggressively retiring shares

• EUR 1.2B cash on hand, zero debt

• 6.8% constant currency revenue growth in Q1 2026

• North America growing 21%, Latin America growing 29%

• Trading around 11 times earnings

So, what is the stock worth? With the S&P 500 at over 30 times earnings and the 10-year treasury around 4.4%, I would be willing to pay at least 20 times earnings for a business of this quality. Using 2025 net income of roughly $1.24B and 199 million shares outstanding, that gives me a buy up to price of roughly $125 per share. With the stock at $67 this remains a massive margin of safety.

However, I have other opportunity costs, and I like to be conservative so let’s say we will pay 15 times last years earnings pay 15 times earnings, that still gets you to $93 per share, nearly 40% above the current price.

Evolution at this price is that it does not need to grow to be a satisfactory investment. At 11 times earnings, buybacks alone would drive meaningful per share value creation for years. Modest to good revenue growth turns this from a good investment to a great one.

Updates Since December

Since I published the original article in December, the story has played out pretty much how I expected, maybe even a little better. Q4 2025 came in solid, the full year results confirmed what we already suspected about earnings power, and Q1 2026 actually delivered higher EPS year over year despite Asia and Europe still being soft. Nothing in the last five months has shaken my thesis, and if anything I understand the business a little better today than I did when I wrote the original piece. The position has grown to nearly 60% of my portfolio and I am buying with any spare cash.

Full Year 2025 Results

Revenue came in at €2,067 million for the full year, basically flat with 2024. Net income was €1,062 million, which optically looks like a 15% decline from 2024, but 2024 was inflated by roughly €151 million in earn out liability reductions that did not repeat. Strip those out and recurring earnings power was just down slightly, essentially unchanged. The buyback program retired 7.3 million shares, or about 3.6% of the share count, at an average price below where the stock trades today. That is exactly the kind of opportunistic repurchasing we like to see when a stock is depressed.

The other thing worth flagging from full year 2025 is that EBITDA (Bullshit earnings but evolution has limited depreciation) margin held above 66% even as revenue went sideways and Asia fell apart. That is the single best proof point that the business model is intact. Pricing power and operational leverage held even with the biggest region under sustained pressure, which tells you the moat is doing its job and the cost structure has plenty of room to absorb regional shocks without breaking the consolidated economics.

Q1 2026 Results

Revenue was €513 million, down 1.5% on a reported basis, but constant currency growth was actually +6.8% in constant currency. The headline decline is almost entirely a currency translation issue rather than business deterioration. Net income was €252 million, down 1.1%. EPS rose to €1.26 from €1.24 a year earlier because the share count is shrinking faster than reported earnings are declining. That is the power of buybacks, and it is exactly the math that makes this stock attractive even if the top line does nothing.

Operating profit was €292.6 million for a 57.0% operating margin, and the net income margin held at 49%. Operating cash flow was €345.8 million, and cash on the balance sheet rose to roughly €1.1 billion. Mobile share of operator gross gaming revenue climbed to 76% from 72%, and regulated markets now make up 48% of total revenue, up from 45%. Both trends are good for long term durability.

From Dividends to Buybacks

The biggest news from the original article is that the board cancelled the 2025 dividend. This caused quite the scare for many investors but I couldn’t have been happier. Management is shifting capital returns toward 100% buybacks. Under the old policy, Evolution paid out about 50% of net profits as dividends, which at the current valuation was a great yield but a worse use of capital than buybacks. The math is straightforward.

At roughly 10x earnings, every dollar the company earns is buying ten cents worth of stock. If they pay that dollar out as a dividend, you get a 10% yield, but you pay tax on it and you do not get any compounding effect on your ownership stake. If they instead use that dollar to buy back stock at 10x earnings, they retire ten cents worth of shares for every dollar spent, growing your per share ownership by roughly 10% for every full year of earnings deployed this way. Over time, if the stock stays cheap, your slice of the pie grows mechanically without the company having to do anything else. And when the stock eventually climbs, every share retired at $65 is worth a lot more on the way up.

The only thing to watch is whether they actually deploy the cash at the same pace they used to send it out as dividends. Something to watch over the next year or so. I hope virtually all income buys back stock.

The Playtech Lawsuit

In October 2025 it was finally revealed that Playtech was the company that hired Black Cube to investigate Evolution and produce the defamatory report submitted to New Jersey and Pennsylvania regulators in 2021. Both U.S. regulators closed their investigations in February 2024 with no enforcement action and explicit findings that there was no evidence Evolution took bets from prohibited jurisdictions. And Carlesund noted on the Q1 call that Evolution has been systematically winning in court for four years now. Whether or not Evolution recovers material damages, the bigger point is that the cloud of suspicion that hung over the stock from 2021 through 2024 has now been turned around and pointed at the competitor who created it. That is a meaningful sentiment improvement even if the financial outcome is small.

Understanding why Playtech would take such a massive legal and reputational risk comes down to the fierce battle for North American market share. Back in 2021, the United States iGaming market was in a state of hyper-growth, and Evolution was rapidly solidifying its absolute dominance in live dealer games across key jurisdictions like New Jersey and Pennsylvania. By attempting to trigger aggressive regulatory investigations, Playtech seemingly hoped to get Evolution’s licenses suspended or fully revoked. Knocking the reigning champion out of the U.S. market would have created a massive revenue vacuum, allowing Playtech to step in, capture those lucrative operator contracts, and permanently alter the balance of power in the B2B casino space.

In terms of a potential windfall, Evolution has publicly stated that the defamatory report caused multi-billion dollar damage to its market capitalization by creating years of artificial regulatory overhang. While successfully suing for stock price fluctuations is notoriously difficult, Evolution is pursuing aggressive claims of trade libel, fraud, and racketeering. If Evolution can prove that Playtech engaged in a coordinated, illegal enterprise to sabotage their business, the court could theoretically award treble damages, meaning the quantifiable financial losses could be multiplied by three. Even if a judge limits the scope to direct legal fees, any provable lost operator contracts, and heavy punitive damages for corporate espionage, a jury verdict or forced settlement could easily reach into the hundreds of millions of dollars. The sheer scale and documented deceit of the operation gives Evolution immense leverage to extract a historic financial penalty.

The true danger for Playtech, however, extends far beyond writing a massive check to their biggest rival. The revelation that Playtech executives actively orchestrated and funded an unethical intelligence operation, allegedly using false identities and secret recordings, has gaming regulators watching very closely. If U.S. gaming commissions determine that Playtech acted with severe moral turpitude or misled authorities regarding their involvement, Playtech could ironically face the very license revocations they tried to inflict upon Evolution. Furthermore, with Playtech’s stock plunging in the wake of the unmasking, the company is now highly vulnerable to class-action lawsuits from its own shareholders for withholding material information about the covert operation and the extreme legal risks attached to it.

Galaxy Gaming Acquisition

The Galaxy Gaming deal, originally announced in July 2024 for about $85 million, has dragged on much longer than expected. The companies extended the outside date to July 17, 2026, they have now secured 5 of the 7 necessary regulatory approvals. They are still working through the remaining state approvals and remain fully committed to closing. However the CEO has noted they will not change the business model to appease Nevada regulators.

I am less confident in the deal then I was initially but at $85 million this is essentially a rounding error for a company that returned €1.1 billion to shareholders in 2025 alone. Galaxy gives Evolution a foothold in physical land based table games and a presence in U.S. omnichannel gaming, both of which are strategically interesting, but neither is critical to the thesis. If the deal closes it’s an interesting positive. If it falls apart it does not really change anything about the business. Here is my seeking alpha article on it.

Regional Breakdown

Evolution reports geography two ways, by where the operator is based and by where the player is actually located using IP address. The player IP view is more useful because it tells you where the actual demand is coming from. By that measure, Q1 2026 revenue split as 39% Asia, 33% Europe, 15% North America, 9% Latin America, and 4% Africa and other.

Asia is still the single largest market by player IP. For full year 2025 the region generated roughly €785 million, about 38% of total revenue. Q1 2026 came in at €197.8 million, down 2.0% year over year but up 2.2% sequentially. That is the second consecutive quarter of sequential growth after a brutal stretch of piracy and cybercrime headwinds. Management was honest on the call that volatility and uncertainty will persist through the rest of 2026, but sequential growth two quarters in a row suggests the worst of the pain may finally be behind us.

Europe has now become the bigger problem. Full year 2025 revenue was approximately €723 million, about 35% of the total. Q1 2026 came in at €167.1 million, down 11.9% year over year and 5.9% sequentially, with revenue levels back to where they were in late 2022. The driver is a combination of regulatory tightening across the U.K., Germany, and Sweden, plus Evolution’s own self imposed ring fencing measures that voluntarily exclude grey markets. Carlesund was explicit on the call that ring fencing was the right long term choice even though the short term cost is high. I agree with him. Europe shrinking from quality driven pressure is an annoying problem but a manageable one. Once the regulatory adjustments stabilize, the regulated European base should be a more durable foundation than what they had before.

North America generated roughly €310 million in 2025, about 15% of revenue. Q1 2026 came in at €75.5 million, up 10.1% in euro terms and 21.4% in local currency, the best growth quarter the region has had since early 2023. The reported euro number is being held back by the weaker U.S. dollar, but the underlying business is accelerating. New Jersey and Pennsylvania remain the anchor markets, but the second Michigan studio just completed construction and Alberta is preparing to launch iGaming. Only seven of fifty states have approved live dealer gaming, which is the long term growth runway I keep coming back to. Every state that legalizes online casino over the next five to ten years is incremental high margin revenue for Evolution, and the regulatory trend is going one direction. This is a massive opportunity.

Latin America also hit an all time high. Full year 2025 revenue was roughly €165 million, about 8% of the total. Q1 2026 came in at €64.4 million, up 29.3% year over year, the fastest growth of any region. Brazil is the standout. The country’s regulated market is now just over a year old and Evolution launched a localized Crazy Time variant that is performing well. They also acquired a studio in Argentina from a competitor that withdrew from the market, and there are further expansion plans in Brazil and Colombia. LatAm is now a real growth engine, not a side project.

Africa and other contributed roughly €83 million in 2025 at 4% of revenue. Small but not zero, and worth watching as smartphone penetration and payments infrastructure improve across the continent.

Live vs RNG Mix

One subtle but important development is that RNG growth is now meaningfully outpacing Live. In Q1, Live revenue declined 3.1% to €434.9 million while RNG grew 8.1% to €78.2 million. For the full year 2025, Live was €1,772.6 million and RNG was €294.0 million, so RNG is now about 14% of revenue and growing.

Live is still the crown jewel, with the moat, the margins, and the scale. But RNG is becoming a real second engine, partly through the NetEnt and Big Time Gaming franchises, and partly because Evolution is using First Person RNG titles as funnels into their Live tables. The new exclusive Hasbro partnership announced last quarter brings 110+ new games scheduled for 2026 release, including multiple Monopoly branded titles spanning both Live and RNG.

Other Items Worth Noting

Customer concentration continues to fall, with the top five customers now representing 39% of revenue down from 46% the prior year, and the largest single customer at about 12%. The total customer base reached around 870 operators after expansion in Brazil. Headcount grew to roughly 22,900, and they added 300 tables during 2025. They now operate 24 studios globally with new builds in Brazil, the Philippines, Romania, New Jersey, and a second Michigan studio. The studio expansion in North America and Latin America in particular is meaningful, since these are the regions doing the heavy lifting on growth, and the Brazil studio specifically should be a real 2026 catalyst now that the country’s regulated market is live.

In short, the underlying business is healthier and more diversified than it was in December, the capital allocation policy got better, the legal overhang is moving in our direction.

Growth Opportunities

The way I think about Evolution’s growth runway, it has two independent dimensions. Geographic expansion, where most of the world’s online casino market is either nascent or still illegal, and product expansion, where Live Casino is the established crown jewel and RNG has room to grow.

By Region

Asia. Long term I expect Asia to grow slowly. It is the largest region by demand and that scale alone provides a meaningful base, but the regulatory picture is fragmented country by country and progress is uneven. China is essentially closed, Japan has discussed expanded regulation for years without clear follow through, and India remains splintered across states. The Philippines is a foothold and a few smaller jurisdictions continue to mature. The cybercrime and stream hijacking issue will likely remain a constant cat and mouse rather than a one time fix. But the directional trend is toward more regulation over time across most of these markets, and Evolution is already the dominant supplier when those markets do open up. Modest single digit growth feels right as a base case, with optionality to the upside if any major market regulates.

Europe. The runway in Europe is the slowest of the four regions in the near term, but the long term picture is more constructive than the recent declines suggest. The current pain is concentrated in three markets and will eventually anniversary, with comparisons getting easier in the second half of 2026. Italy and Spain continue to grow at healthy rates, and several European markets are still in the early stages of regulating online casino. The Netherlands regulated in 2021 and is still maturing. Once the worst of the ring fencing effects laps, the European base should stabilize at a level that is more durable than it was before, since what remains will be almost entirely regulated and licensed. Long term Europe should return to modest low single digit growth, but it still might be a few years from stabilizing.

North America. This is the single highest conviction growth opportunity in the entire portfolio. Online casino is currently legal in only seven U.S. states: New Jersey, Pennsylvania, Michigan, West Virginia, Connecticut, Delaware, and New Hampshire. That is seven of fifty. Sports betting is now legal in over thirty states and the trajectory of online casino legalization tends to follow sports betting with a five to ten year lag. Every new state that legalizes is incremental high margin revenue for Evolution since they already dominate the live dealer category in the states that have legalized. New York has been debating online casino for years and budget pressure could finally push it through. Maryland, Illinois, Massachusetts, and Indiana all have legislation introduced. Even one major state legalizing would be a meaningful event. Alberta is also preparing to launch iGaming this year, opening a second Canadian province after Ontario. Layered on top is the Galaxy Gaming acquisition, which gives Evolution a presence in physical land based table games and an omnichannel bridge between brick and mortar casinos and online.

To put the math behind that ten year trajectory, North America generated roughly €310 million in 2025 primarily on the back of just seven legal jurisdictions. That translates to an average yield of roughly €44 million per regulated state. If the legal state count reaches twenty over the next decade, applying that same average pushes North American revenue to roughly €880 million annually. That baseline projection is likely conservative because the current average is dragged down by smaller populations in places like West Virginia, Delaware, and New Hampshire. If major legislative dominos fall in densely populated states like New York or Illinois, the revenue per state average would increase significantly. This math also completely excludes incremental growth from Canadian expansions like Alberta.

When you compare that €880 million baseline projection to the rest of the business, the thesis solidifies. Asia, currently the largest market by player IP, is running at an annualized rate of roughly €800 million. By simply adding thirteen average sized states over a ten year horizon, North America mathematically overtakes the current leader to become the biggest driver of the business.

Latin America. The runway here is excellent. Brazil has a population of over 200 million and a gambling culture that is finally being served legally for the first time. Colombia is the next expansion target with new studio capacity planned. Mexico is an even larger potential opportunity if and when regulation matures, though that is a longer dated catalyst. I expect LatAm to grow at a healthy double digit clip for three to five more years before settling into mid single digit growth as it matures. Over a decade, this could be a €500 to €700 million revenue region, two to four times its current size.

Africa. South Africa is already a regulated market and Evolution holds a license there. The continent is in the very early stages of digital gambling adoption. Not modeled into the thesis, but not zero over a ten to twenty year horizon.

By Segment

Live Casino. Live Casino remains where Evolution has the deepest moat. The growth here is going to come from three sources. First, raw volume growth as more players come online globally, which is the geographic story above. Second, new game formats and game shows, where Evolution has consistently been able to launch hits that command premium economics. Crazy Time, Monopoly Live, Lightning Storm variants, these are not commodity products, they are entertainment franchises, and Evolution is the only company with the studio infrastructure and creative depth to produce them at scale.

Third and most important is the Hasbro partnership. Evolution has the exclusive worldwide license for Hasbro intellectual property in live and online casino content, which means Monopoly is just the beginning. Battleship, Risk, Trivial Pursuit, Game of Life, and dozens of other Hasbro brands are now potential game show formats. Management announced 110+ new game launches for 2026 alone, with multiple Monopoly titles spanning both Live and RNG. This is the most aggressive product roadmap in the company’s history and it goes directly through the highest margin part of the business.

Looking forward, mapping out the growth trajectory for Live Casino requires accepting a basic mathematical reality. Evolution’s current market share of roughly 60% is simply too high to hold forever. When you command that much of the live dealer space, the only direction for market share to go is down as the industry matures and well capitalized competitors fight for operator floor space. However, that shrinking slice of the pie is offset by the pie itself is multiplying in size. The global total addressable market for live dealer gaming is expanding at a rapid clip, driven by the ongoing shift from physical to online casinos and the opening of new regulated jurisdictions. Even if Evolution slowly cedes market share over the next decade, the sheer volume of new players entering the ecosystem should easily support sustainable mid single digit revenue growth for the segment.

It is a highly competitive environment, and the barriers to entry for launching basic baccarat or blackjack tables are lower than they were five years ago. But basic tables do not drive the premium economics or player retention that operators demand. Evolution remains the clear leader because their scale, studio infrastructure, and exclusive intellectual property create a product offering that cannot be easily replicated by newcomers. They are no longer just competing on providing video feeds to card shoes, they are competing as an entertainment and broadcasting powerhouse, making their position at the top of the food chain highly defensible and making a mid single digit growth baseline highly achievable even as rivals chip away at the edges.

RNG. RNG is becoming the more interesting growth story in the near term because it is growing faster than Live and the comparisons are easier. The brands inside the portfolio include NetEnt, Big Time Gaming, Red Tiger, and Nolimit City, all acquired and now contributing meaningful revenue.

There are a few reasons I think RNG continues to outgrow Live for the next several years. First, RNG titles are easier to launch in new geographies because they do not require building physical studios with live dealers, making them the natural first product into emerging markets. Second, First Person RNG titles are proving to be effective funnels into the Live tables, so the two segments are increasingly complementary rather than competitive. Third, the Hasbro partnership produces RNG content as well, and slot style Monopoly titles will likely launch faster than full live game shows.

The contrast with Live is instructive. In Live, Evolution is defending a massive 60% market share, meaning growth relies almost entirely on the overall market pie expanding. RNG is the exact opposite. The global slots and digital table games market is highly fragmented, and Evolution holds only around an 8% market share in this category. That gives RNG a dual growth engine. Not only does it benefit from the same structural tailwinds of the overall iGaming market getting bigger, but it also has immense runway to actively take market share away from legacy slot providers. They do not need to defend the crown here, they get to play offense. RNG also comes with even better margins than live, once you create a slot machine incremental costs are neligible.

Putting It All Together

When you step back and look at the full picture, Evolution has at least three independent growth vectors firing at different stages of maturity. North America is in the early innings of a decade long legalization wave, with only seven of fifty states live and an average yield of €44 million per state that understates the potential of big population markets still waiting in the wings. Latin America is a year into Brazil’s regulated market and growing nearly 30% with Colombia and eventually Mexico ahead of it. And RNG is a low market share segment with a dual engine of industry growth plus share gains, turbocharged by the Hasbro IP pipeline.

Asia provides a massive revenue base with modest upside from incremental regulation, and Europe should eventually stabilize once the ring fencing and regulatory adjustments anniversary. Neither needs to be a growth hero for the thesis to work.

The realistic base case over the next five to ten years is mid to high single digit consolidated revenue growth, driven primarily by North America and Latin America on the geographic side and RNG on the product side, with Live Casino grinding higher on TAM expansion even as market share normalizes. The bull case, where multiple large U.S. states legalize in quick succession and Brazil scales faster than expected, could push consolidated growth into the low double digits for an extended stretch. Either scenario is more than sufficient at a stock trading around 11x earnings with a management team actively buying back shares.

Risks

The biggest risk to this business is competition in the Live segment, specifically the threat of Pragmatic Play taking market share and compressing margins. Evolution’s Live Casino margins are extraordinary, but that kind of profitability naturally attracts well capitalized rivals. Pragmatic Play is the most serious challenger here. They are private, backed by a larger gaming group, and have been aggressively attacking the live dealer space by pricing below Evolution and releasing content quickly. While they are not going to dethrone Evolution, they have been winning share at the margins with smaller and mid sized operators in Europe and LatAm. The real danger is not that Pragmatic takes over the industry, but that they become credible enough to force Evolution to compete on price, which would act as a ceiling on how much Evolution can lean on pricing power and slowly erode those premium margins over time.

Playtech is the other notable competitor, though I view them more as a legacy player than an active operational threat. They have been around forever and run a broader B2B platform business, but their live dealer product simply has not kept pace with Evolution on innovation, content cadence, or studio quality. Playtech is a slow fader, and the real action in their corporate story is the lawsuit with Evolution that I covered earlier.

Beyond those two, there are smaller players like BetGames and Authentic Gaming, plus a handful of regional operators, but nobody at scale. The moat in live dealer is real and incredibly deep. You need physical studios in regulated jurisdictions, hundreds of trained dealers per studio running around the clock, the tech stack to broadcast and integrate with operators, the licenses, the content library, and the operator relationships. Evolution has been building this for fifteen years and the gap is wide. Even Pragmatic Play, the most aggressive challenger, is much smaller relative to Evolution.

The tell on their competitive position is that Evolution’s market share has held at roughly 60% for years, even as Pragmatic Play has poured capital into the space and even as the overall pie has gotten much bigger. Holding share while the market rapidly grows is difficult thing for a market leader to do, and they have successfully done it.

Because the competitive moat is so well established, I actually view regulation as a secondary risk, largely because Evolution’s exposure is deeply mitigated by its geographic spread. However, Evolution operates in over 100 jurisdictions across every populated continent. No single country represents a threat large enough to break the business. When Asia cratered in 2025, the rest of the company kept producing. When the UK tightened affordability checks, other European markets picked up the slack. That geographic spread is one of the reasons I am willing to size this position so large. If Evolution were 100% UK or 100% US revenue, It would be a much smaller position. The fact that revenue is genuinely scattered across the globe means a regulatory shock anywhere becomes a temporary headwind, not an existential problem.

Two regulatory areas I pay close attention to are Europe and the USA, and they represent very different types of risk. Europe is a large market where regulation is hurting Evolutions revenue growth. The UK, Sweden, Netherlands, and Germany have all moved toward tighter rules over the last several years with stake limits, deposit caps, and advertising restrictions. Evolution has navigated this well so far, partly by working only with licensed operators and partly because the live dealer experience is less of a regulatory target than slot machines. But Europe is still down 12% year over year and represent a meaningful chunk of revenue. Regulations across the continent acts as a constant drag on growth.

The US is the opposite kind of risk. The risk there is not that current iGaming states tighten rules, it is that legalization in new states slows down or stalls completely. The upside of the growth thesis depends on more states opening up over the next decade, and that is not guaranteed. State legislatures are unpredictable and anti-gambling sentiment is real in many parts of the country. If the US gets stuck at the seven states it has today and never expands, my growth case weakens. The base case still works fine because the existing states keep growing, but the massive upside scenario relies heavily on US expansion playing out.

So when I think about risks, the summary is that regulation could compress growth in Europe and slow the US opportunity, while competition will keep nibbling at the edges and testing their pricing power. Neither one is a thesis killer. I actually think regulations add more to the moat than it hurts, it’s very difficult to be a newcomer in this space because of all the regulations.

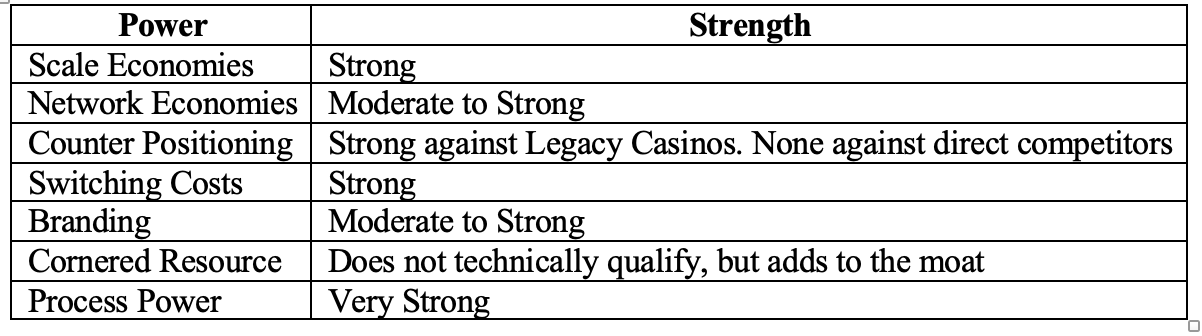

How Big Is The Moat? Huge

I did the 7 powers in my initial post but I think it is important enough to repeat.

Warren Buffett often talks about the moat of a company. Every business is like a castle and in order to protect the castle you need a strong moat to keep competitors from storming the castle and taking your customers away.

Hamilton Helmer’s book 7 Powers takes Buffett’s castle and moat idea and breaks it down into seven specific strengths called powers. According to Helmer, every lasting business needs at least one of these powers. If it doesn’t have one, competitors will eventually wear it down and eat away at its profits. The more powers a company has the bigger and stronger their moat.

The seven strategic powers are:

Scale economies: producing at lower cost as volume grows

Network effects: products that become more valuable as more people use them

Counter positioning: taking a strategy incumbents can’t easily copy

Switching costs: barriers that make customers hesitate to leave

Brand: emotional connection and trust that support pricing power

Cornered resource: exclusive access to something valuable

Process power: unique ways of operating that are hard to replicate

Evolution has six clear powers and a strong case for a seventh, which is extraordinarily rare and the single biggest reason I am willing to size this position the way I have.

Scale Economies

A live casino studio is a massive fixed cost. You build the studio, install the cameras and lighting, staff the tables with dealers, pit bosses, and IT, and run it 24/7. Once the studio is built, the cost of serving the millionth player is roughly the same as serving the hundredth. Evolution’s Common Draw technology takes this even further by letting one dealer serve hundreds of thousands of players at once, instead of seven players at a physical table. Their cost per player approaches zero as they scale, while a smaller competitor has the same fixed costs spread over a fraction of the volume. That is why Evolution earns 50% net margins and competitors earn far less, and it is why competitors cannot price below Evolution without bleeding cash.

Network Economies

This one is real but it is important to be precise about what kind of network effect it is. This is not a consumer network effect like Visa or Facebook where each new user directly makes the product better for every other user. It is a B2B flywheel. As more major operators like FanDuel, BetMGM, and DraftKings plug into Evolution, the company collects more data, generates more cash to fund new game development, and produces more exclusive content like the Crazy Time and Lightning game shows. Players actively look for these specific titles, which means new operators have to carry Evolution to stay competitive in their lobby. More operators bring more players, more players justify more content, more content pulls in more operators. A new entrant cannot break into this loop without already being inside it. It is not a pure network effect in the textbook sense, but the flywheel dynamic creates a very similar result, and as a practical matter the competitive advantage it produces is just as real.

Counter Positioning

Evolution had this power early on and it is the reason they exist at the scale they do today. In the early years, Evolution was building capital light digital infrastructure while MGM, Caesars, and the rest of the legacy casino industry were busy protecting their multi billion dollar physical assets and hotel revenue streams. The legacy casinos could not copy the model without cannibalizing their own foot traffic and stranding their real estate investments. By the time the legacy giants realized the market was moving online, Evolution already had a decade long head start. That is textbook counter positioning.

The important nuance is that this dynamic is still playing out, but only against legacy casinos in markets that have not yet regulated online gambling. Every time a new state or country opens the door to online live dealer, the existing brick and mortar operators in that market face the exact same cannibalization dilemma, and Evolution is positioned to be the picks and shovels supplier the moment the digital channel opens up. With only 7 of 50 U.S. states currently allowing online live dealer, there is a long runway of new markets where this advantage keeps repeating.

Against Evolution’s actual direct competitors, Pragmatic Play, Playtech, and the other online live casino providers, counter positioning does not apply. Those businesses are structured the same way Evolution is, just smaller. There is no business model conflict preventing them from copying what Evolution does, and they are trying. The reason they cannot catch up has nothing to do with counter positioning and everything to do with Scale Economies and Process Power. That distinction matters because it tells you where the real competitive threat lives and which powers are doing the defensive work against it.

Switching Costs

Operators integrate Evolution’s games through an API, train customer service staff on the products, run marketing campaigns built around specific Evolution titles, and build entire sections of their casino lobbies around Evolution content. Crazy Time and Lightning Roulette are not just games on a menu, they are headline products that operators promote and that players come looking for. Pulling Evolution out and replacing it with Pragmatic would mean reintegrating, retraining, remarketing, and risking that the players follow the games to a competing site. Most operators would rather pay the higher rev share than deal with the friction. The switching costs are not as high as enterprise software, but they are real and they create stickiness in the operator base.

Branding

The Evolution corporate brand does not really matter to most end players, who mostly do not know they are playing on Evolution infrastructure. But Crazy Time, Lightning Roulette, Monopoly Live, Funky Time, and the rest of the game show portfolio are real consumer brands that players actively search for and that operators use to drive traffic. The new Hasbro deal extends this with a multi year IP partnership built around brands that have global recognition without any work required. Operators pay Evolution a premium revenue share partly because they need these titles to keep their highest value customers happy. So, the brand power lives at the title level rather than the corporate level, and at that level it supports real pricing power on the marquee titles and helps with marketing pull through.

Cornered Resource

This one does not technically qualify as a cornered resource under Helmer’s strict definition. A true cornered resource is exclusive access to something a competitor literally cannot obtain, like a patent, a unique mineral deposit, or a one of a kind dataset. Evolution does not have that. But in my mind what they do have still adds meaningfully to the moat and is worth calling out. They hold gambling licenses in dozens of jurisdictions, many of which took years to obtain and required significant legal and operational investment. The Galaxy Gaming acquisition, when it closes, brings 131 licenses across 28 U.S. states and the intellectual property for popular table game side bets used in physical casinos. On the talent side, the product team led by Todd Haushalter has built a creative monopoly on live game show formats that competitors have not been able to replicate at the same quality or cadence. None of this is exclusive in the way Helmer means, a well funded competitor could eventually get the licenses and hire talented game designers, but the combined regulatory and creative position is something that would take years and hundreds of millions of dollars to replicate. It is not a power in the formal sense but it is absolutely a contributor to the width of the moat.

Process Power

This is the one I think is most underrated, and it is probably the strongest moat Evolution has. Live casino is an operating business, not a technology business, despite the broadcast tech. You need to run dozens of studios in regulated jurisdictions across multiple time zones, hire and train hundreds of dealers per studio, design and ship new games on a regular cadence, manage the content pipeline, broadcast in dozens of languages, integrate with hundreds of operators, maintain uptime, handle disputes, and stay compliant with shifting regulation in every market. Evolution has been doing this for fifteen years. They have built up the institutional knowledge, the playbooks, the dealer training programs, the studio buildout templates, and the regulatory relationships. A competitor with infinite capital still cannot buy fifteen years of operational learning. This is why Pragmatic Play, despite being well funded and aggressive, has been chasing for years and is still a clear number two.

Power Summary

Five powers doing the real defensive work, a partial sixth in cornered resource, and a counter positioning dynamic that still has runway but only against legacy operators in markets that have not yet opened. Against Evolution’s actual direct competitors, what is holding the line is Scale Economies, Network Economies, Switching Costs, Branding, and Process Power. The two strongest, Scale Economies and Process Power, are the hardest to replicate.

When Buffett talks about a moat, he is really asking one question. If you handed a competitor a billion dollars and told them to come destroy this business, could they do it? With Evolution the answer is no, and the reason is not any single power on its own but the way they reinforce each other. Scale Economies make the unit costs unbeatable. Process Power means even if you copied the model exactly, you still cannot copy fifteen years of operational learning. Switching Costs lock in the operators you would need to peel away to grow. Branding at the title level gives Evolution pricing power on the games that matter. The network flywheel keeps pulling in more operators and more players, which funds more content, which pulls in more operators. A new entrant has to attack all of these at the same time, using capital that has to compete against a business already earning 50% net margins. That is a moat in the truest sense, not a single barrier but a layered defensive position that gets wider every year the business keeps operating.

This is also the quality dimension Munger always emphasized. He would say it is far better to buy a wonderful business at a fair price than a fair business at a wonderful price, and what makes a business wonderful is precisely what Evolution has. Returns on invested capital compounding at high rates without much reinvestment required. Durable pricing power on the products that matter most. A customer base that cannot easily leave. A competitive position that strengthens with scale rather than diluting. Evolution does not need to do anything heroic to keep earning these returns. They just need to keep doing what they have been doing, which they have demonstrated they can do for fifteen years through multiple regulatory cycles, competitive waves, and macro environments. The kind of business where the right answer is usually to sit still and let the compounding happen.

And yet the stock trades at roughly 11 times earnings. The market is pricing Evolution like a deteriorating commodity business rather than the kind of compounder Buffett and Munger spent their careers hunting for. That mispricing is what creates the opportunity. When you can buy a business with this kind of moat, this kind of profitability, and this kind of management discipline at a multiple normally reserved for cyclical no growth industrials, the only real question is whether you are seeing something the market is not. I have spent enough time on the licensing situation, the Asia headwinds, and the regulatory overhang to be comfortable that the answer is yes. That is what makes the 11x multiple so strange and what gives me the conviction to size this the way I have.

Stock Outlook

For me to put 60% of my portfolio in a single stock, the risk reward has to be heavily in my favor. I think it is, and the rest of this section walks through why. I once had 90% in Dick’s Sporting Goods, that article is here.

When I look out ten years, I believe the chance of an actual loss in this stock is very low, somewhere below 1%. For me to lose money, the business would have to deteriorate in a meaningful way. Revenue would have to stop growing and start declining, margins would have to evaporate, the moat would have to crumble. It is genuinely hard for me to picture how that happens. The growth opportunities are spread across too many regions, the regulatory risk is too diversified, and the competitive position is too entrenched. I would have to be wrong about almost everything to lose money over a decade.

The thing that protects the downside even in a bad scenario is the buyback math. At around 10x earnings, management can retire roughly 10% of the company every year using the entire profit stream. That is the math when your earnings yield is 10%, every dollar of net income buys back 10 cents of market cap. Even if earnings fell, the buyback alone would prop up the stock price. Here is the most extreme version of this. Imagine in 2036 net income has fallen in half and they have bought back half the company over the decade. Earnings per share would be unchanged from today, and at the same 10 P/E the stock would be sitting right where it is now. You would have made nothing, but you would not have lost anything either. This is the disaster scenario I can create and it would take a monumental fail from management and worldwide gambling regulations.

Worst Case

In this scenario almost everything that could go wrong does go wrong. Asia never recovers and gets worse, with regulators in multiple countries effectively shutting down the gray market access points and cutting Asia revenue by more than half. Europe tightens dramatically, the UK extends affordability checks to live casino, Sweden and Germany follow with similar rules, and European revenue per player drops materially. Pragmatic Play and Playtech finally close the gap on game quality and start winning material share at the operator level, forcing Evolution into rev share concessions for the first time in its history. The Hasbro deal underwhelms, the new game show formats fail to produce another Crazy Time, and the creative engine that has driven the brand power slows down. US state by state legalization stalls out at 8 or 9 states as anti gambling political pressure builds. Margins compress from 50% net to something closer to 30% as pricing power erodes and regulatory compliance costs rise. Earnings fall in half over the decade. Even in this scenario, management buys back half the company along the way, EPS holds steady, the multiple stays at 10x, and the stock price ends up about where it started. You make nothing for ten years. This is dead money, not a loss. I cannot picture this actually happening, but it is the floor.

Bad Case

The business stagnates without breaking. Asia weakness persists longer than expected, the recovery I am betting on takes 4 or 5 years instead of 1 or 2, and Asia ends up a smaller piece of the business than it is today. Europe sees gradual margin compression from regulation but no outright collapse. US legalization continues at the slow pace it has been on, maybe 2 or 3 new states opening up over the decade rather than the dozen the bull case requires. Pragmatic gains some operator share but Evolution holds the marquee titles and the highest revenue accounts. The Hasbro deal produces decent but not great content. Margins drift from 50% to maybe 42% as competition takes a bit of pricing power. Net income in 2036 looks roughly the same as today. The business does not break, it just does not grow. In this scenario, ongoing buybacks shrink the share count by roughly 6 to 7% per year on average, EPS compounds even with flat net income, and the stock delivers something like a 7% CAGR at a 10 P/E. Not exciting, but not a disaster either. You earn a market like return without any operational improvement at all.

Base Case

Growth resumes at a moderate pace. Asia stabilizes over the next year or two as the company adjusts its market access strategy and the regulatory picture clarifies, with Asia returning to modest growth by 2027 or 2028. US legalization continues at a steady clip, with 6 to 10 new states opening up over the decade including at least one large one like New York or California, expanding the addressable US market by several multiples. Europe stays slow but functional, the regulatory environment is challenging but predictable, and Evolution holds its dominant position with its existing operator base. Pragmatic remains a clear number two and never seriously threatens Evolution’s premium positioning. The Hasbro deal produces a few solid hits even if nothing matches Crazy Time. Margins hold around current 50% levels as scale economies offset modest pricing pressure. Galaxy Gaming closes and adds a small but profitable land based revenue stream. Revenue grows in the mid to high single digits annually. Buybacks continue at a strong pace, and the market eventually re rates the stock to something like 15 to 18x earnings as the growth story comes back into view. EPS roughly doubles or triples over the decade, the multiple expands modestly, and the stock returns somewhere in the 10 to 20% CAGR range depending on Mr. Markets PE ratio.

Bull Case

Everything works. Asia recovers cleanly within 18 months as the regulatory issues prove temporary and the underlying player demand was never the problem. US legalization accelerates dramatically as states facing budget pressure look for new revenue sources, with 12 or more new states opening up including the big ones, and the US becomes Evolution’s largest market by 2030. Brazil opens up under its new regulatory framework and becomes a major growth driver, India eventually follows, and the addressable market expands by orders of magnitude. The Hasbro IP deal produces a breakout hit on the level of Crazy Time, extending the brand power and the title level pricing premium. Galaxy Gaming proves to be a brilliant acquisition that gives Evolution a meaningful land based business and exclusive side bet IP that competitors cannot touch. Pragmatic and Playtech fall further behind as Evolution’s scale advantages compound. Margins actually expand back toward 70% EBITDA as the new market growth comes through with very high incremental margins. Management continues to buy back shares aggressively at low multiples before the market catches on, supercharging per share results. Revenue grows in the low to mid teens, EPS quadruples or more over the decade, and the multiple re rates to 20 to 25x as Evolution becomes recognized again as a quality compounder. The stock delivers a 25 to 30% CAGR.

The Asymmetry

The downside is dead money in a worst case I cannot really picture, and a roughly 7% CAGR in a bad case where the business simply stagnates. The base case is a 10 to 20% CAGR. The bull case is a multi bagger. There is no scenario I can construct where I actually lose money over ten years that does not require the business to fundamentally break in ways the moat seems to prevent. That is what asymmetric means. The downside is bounded by buybacks at a cheap multiple. The upside is open ended. When you find that combination on a business of this quality, the rational response is to buy as much as you can

That is why this is 60% of my portfolio.

Models

I’m not a big model guy. I agree with Warren Buffett when he says an investment should be so good it hits you in the face. I don’t need to run a giant DCF model to decide if a stock is cheap or not. The minute you find yourself torturing a spreadsheet to make the numbers work, the answer is no.

With that said, I do run two models. One is a mental model. The other is an Excel model I built. I don’t use either to make decisions. I do it mostly for fun, and it’s fun to look at and look back on years later to see how reality compared to my assumptions.

The Mental Bond Model

Warren Buffett said investing in stocks is the same as investing in bonds. You just have to write the coupon on the stocks yourself. That one sentence reframes everything. A bond promises you a stream of coupons over time. A stock does the same thing, except the coupons grow if the business grows and shrink or disappear if it doesn’t. Your job as the investor is to figure out what those coupons will look like and then decide if today’s price gives you a fair shake.

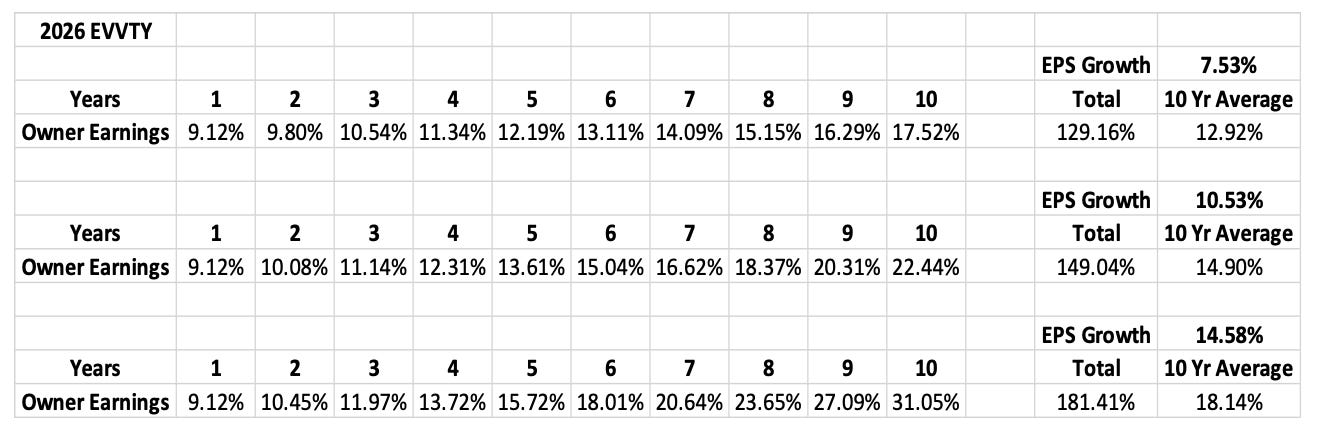

Here’s how I mentally create a 10 year bond for Evolution. First I think about net income growth and share buybacks averaged over the next 10 years to get an EPS growth rate. Then I add that growth rate to the current earnings yield. The earnings yield is just the inverse of the PE ratio, and it tells you what percentage of the purchase price the business is earning for you today. Add EPS growth on top and you have a rough approximation of what your stock bond will pay you each year if Mr. Market leaves the multiple alone.

Again, this is just a tool, not how I actually make decisions. Thinking about the business and its future is far more important than any model.

Using this model in the low growth scenario, where net income grows 0% but buybacks run at 7% due to the low stock price, the bond averages 12.92% a year. Notice that I assume fewer buybacks in the higher growth scenarios. That isn’t a quirk, it’s the math. Higher growth would push the stock up and make every buyback dollar retire fewer shares. Buybacks become less powerful precisely when the market wakes up. The conservative case actually gets a boost from a sleepy market, which is one of the more elegant features of a cannibal stock trading below its worth.

I believe the assumptions I used are conservative, but I like to be conservative in estimates. I’d rather be pleasantly surprised on the upside than caught off guard on the downside.

Obviously in my head I can’t get these results to the hundredth decimal point 10 years out, but with those numbers I can reasonably estimate the values within a percentage point or two on either side. That’s plenty of precision for the decision at hand.

When you can find a situation where your worst case scenario delivers a 13% annualized return, you don’t tiptoe in. That’s when you bet big. That’s when you put 60% of your portfolio in it.

The Excel Model with Mr. Market

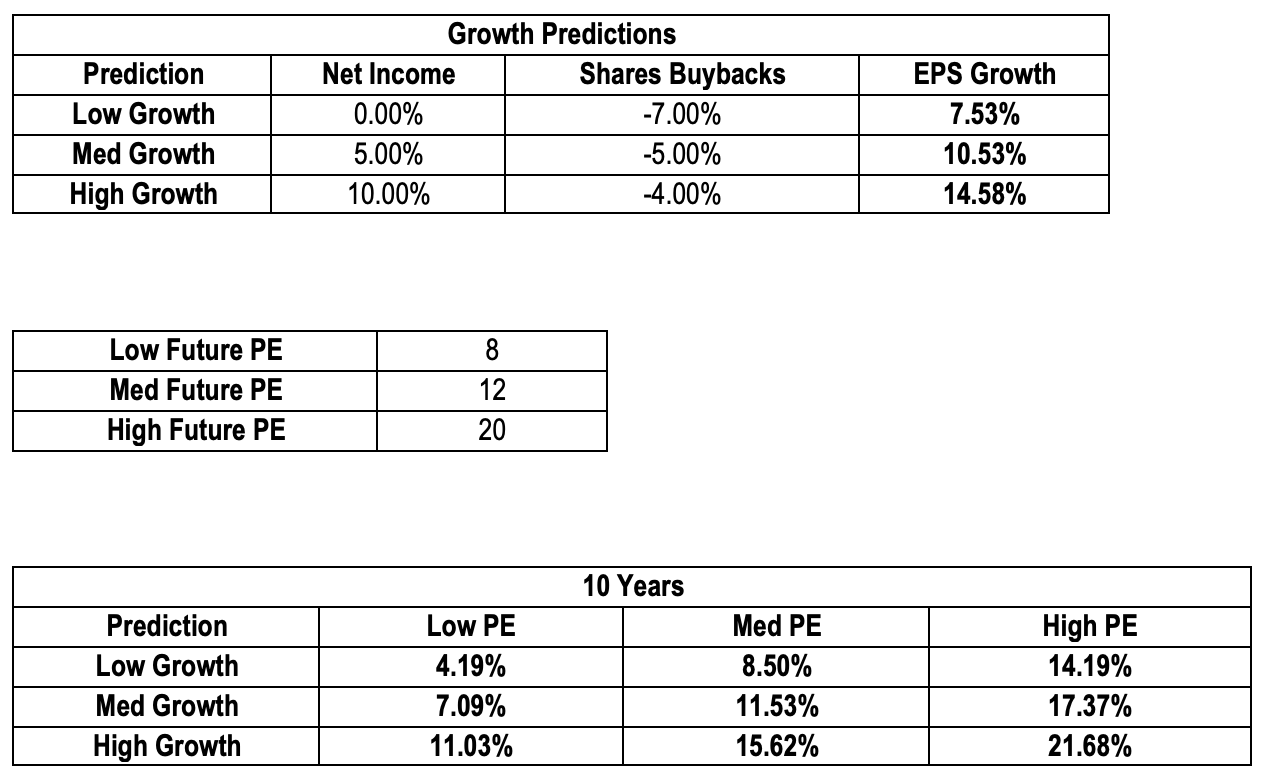

This next one I actually build in Excel, but again, just for fun. It uses the same growth assumptions, only this time it factors in Mr. Market and his crazy moody swings in PE ratio. Ben Graham’s old parable still holds. Mr. Market is your manic depressive business partner who shows up every day offering to buy your share or sell you his at wildly different prices depending on his mood. The first model assumed Mr. Market was on lithium and left the multiple alone. The second model lets him swing.

Taking Mr. Market into account, you can see the worst scenario delivers a disappointing 4% return, while the best clocks in north of 21%. Again, I believe these numbers are conservative, especially on the buyback side. At 11 times earnings, I expect Evolution to retire 8% or more of its shares this year alone. The lower the price goes, the more shares come off the table, and every remaining share gets a bigger slice of the same earnings pie. That’s the part Mr. Market never seems to price in correctly when he’s depressed.

Now look at the shape of this distribution. The worst case is a positive 4% return. Not great, but you’re still ahead of inflation in most environments, and you got there assuming both zero net income growth and a PE compression all the way down to 8 times earnings. That requires Evolution to essentially stop growing while the market simultaneously decides it’s a melting ice cube. Both can happen. Both happening together for ten straight years is a stretch. The medium case lands in the 11 to 15% range, which is a perfectly respectable long term equity return. The high case is north of 21%, which would put Evolution alongside the great compounders of the last few decades.

This is the asymmetry Buffett and Munger spent their entire lives hunting for. Heads I win a lot, tails I likely still beat the market. When the floor of your reasonable outcomes is a positive return and the ceiling is a multibagger over a decade, the decision isn’t hard, it’s obvious. You don’t agonize over a position like this. You don’t trim around the edges and call it risk management. You don’t wait for a better entry that may never come. You sit on your hands when nothing fits, and you back up the truck when something like this shows up. Charlie Munger said it best. The big money isn’t in the buying and the selling, it’s in the waiting. I live for setups like Evolution, and now that it’s in front of me I’m not going to be cute about position sizing. That’s why it’s my largest holding, and it’s why I keep adding every time I get spare money.

Conclusion

Not much has changed since December and that is exactly the point. The business is still the dominant infrastructure layer for live dealer gaming, the margins are still extraordinary, the moat is still as wide as anything I follow, and the stock is still trading at 11 times earnings. The only real difference is that I understand the business better today than I did four months ago, and the position has grown to nearly 60% of my portfolio.

The way I see it, you are getting a market leader with 60% share, 50% net income margins, 1.1 billion euros of cash on the balance sheet, zero debt, growing 7% in constant currency, retiring shares at a record pace, and pushing into the largest under penetrated growth markets in the world. North America is hitting all time highs, Latin America is hitting all time highs, Asia is showing two consecutive quarters of sequential improvement, and management is using every available euro to shrink the share count at a price that mathematically does not make sense for a business of this quality.

At 10 times earnings, you do not need this story to play out perfectly to make money. You barely need it to play out at all. Buybacks alone could get you to a market like return if revenue went sideways for a decade. Any actual growth, in any region, in either segment, is upside on top of that. And the long term setup, with US legalization in early innings, Brazil just getting started, the Hasbro pipeline kicking off, and Asia still having optionality, looks like the kind of asymmetric bet you build a portfolio around.

I have been investing long enough to know that opportunities like this do not come along often. A dominant business, with a wide moat, growing in three of four regions, returning massive capital to shareholders, and trading at 10 times earnings. That combination is what makes me willing to put nearly 60% of my portfolio behind it. I will keep adding aggressively to my portfolio until maybe $80 a share. Not because I think it’s overpriced but because I have most of my net worth in it and might be time to diworsify. Until then I will keep adding see how many shares I can get. I hope the stock trades down for years to come.

Disclaimer

Disclosure: At the time of this writing, I hold a long position in CROX. This article is for informational and educational purposes only and should not be construed as professional financial advice.

Investing in individual stocks involves significant risk, including the potential loss of principal. I am not a registered investment advisor or a broker-dealer. Readers should conduct their own due diligence or consult with a qualified financial professional before making any investment decisions. While I strive for accuracy, all data is provided “as is” and is subject to change without notice.

FWIW Capital allocation has generally been viewed as a negative for EVO not a positive due to poor m&a. Also, what do you think about the risk to polymarket and kalshi to the gaming market? Feels like those guys are killing it right now.

This took quite a bit of effort to write and I appreciate that. I do wish to caution you a bit. There is language in here that gives me the impression that you're trying to convince yourself. To wit:

1) "a perfect business model"....No business model is perfect.

2) "capital allocation is superb".....That's an opinion and nothing more.

3) "Heads I win a lot, tails I likely still beat the market. When the floor of your reasonable outcomes is a positive return and the ceiling is a multibagger over a decade, the decision isn’t hard, it’s obvious.".....Whoa! That's hyperbole. The floor to any business 10 years forward is impossible to quantify. Things can happen which we would never consider in our analysis.

All I'm saying is that you should be careful. 90% in one stock and now 60% in another stock is extremely risky. Your success in the first may cloud your thinking. Neither one is a diversified business.

Best of luck.